If you have built a pension pot of £250,000 and are starting to think about whether it is enough to retire on, you are asking exactly the right question. The honest answer is that it depends. £250,000 can support a frugal retirement comfortably, particularly if you also receive the State Pension, but it falls short of what most people would consider a ‘comfortable’ retirement on its own. Whether it is enough for you depends on three factors: when you retire, what other income sources you have, and what kind of lifestyle you want to maintain.

This guide walks through what £250,000 actually buys in retirement, how the State Pension affects the picture, the difference between annuity and drawdown approaches, and what you can do if your pot is currently below the level you need.

In my practice, conversations about retiring on £250,000 typically begin with a mixture of optimism and quiet anxiety. Clients often arrive having read headlines suggesting this figure is ‘enough,’ and are surprised to learn that, on its own, it usually supports a frugal rather than comfortable lifestyle, particularly before the State Pension begins. The broader picture I encourage clients to consider is not just the size of the pot, but the interplay between withdrawal rate, retirement age, other income sources, and the lifestyle they genuinely want, because these factors, more than the headline number, determine whether retirement feels secure.

Table of Contents

ToggleHow much income does £250,000 actually provide in retirement?

The standard rule of thumb in UK retirement planning is the 4% rule, originally developed by US economist William Bengen in 1994. Bengen analysed 50 years of historical market data and concluded that withdrawing 4% of your initial pension pot per year, adjusted for inflation, was likely to make a portfolio last 30 years across the majority of historical market scenarios.

Applied to £250,000, the 4% rule produces an annual income of £10,000. Adjusted for typical UK retirement realities (where most people take 25% as a tax free lump sum first), the picture looks slightly different. Taking £62,500 as a tax free lump sum leaves £187,500 invested, generating £7,500 per year at a 4% withdrawal rate.

Alternatively, you can use £250,000 to buy an annuity, which converts the pot into a guaranteed income for life. At current annuity rates (mid 2025 to early 2026), a 65 year old buying a single life, level annuity from £187,500 (after taking the tax free lump sum) would receive approximately £14,000 per year for life. The trade off is that this income is fixed in nominal terms (an inflation linked annuity provides less starting income but rises with prices), and there is no residual capital to pass on.

Drawdown offers more flexibility but exposes you to investment risk. Annuity offers certainty but no flexibility and no inheritance value. Many retirees use a blended approach: part annuity for security, part drawdown for flexibility.

The State Pension makes a meaningful difference

The new State Pension for 2025/26 is £230.25 per week, or £11,973 per year. This is paid to anyone who has accrued 35 qualifying years of National Insurance contributions, and it begins at State Pension age (currently 66, rising to 67 between 2026 and 2028).

Adding the full State Pension to a £250,000 pot using the 4% rule produces a total annual retirement income of approximately £22,000 per year. This is a meaningful uplift from the £10,000 the pension pot alone provides.

If you have been contributing National Insurance throughout your working life, you will likely qualify for the full or near full State Pension. It is worth checking your State Pension forecast on the government website at gov.uk/check-state-pension before assuming the full amount, as gaps in National Insurance contributions can reduce the entitlement.

What does the Pensions and Lifetime Savings Association say is enough?

The Pensions and Lifetime Savings Association (PLSA), in conjunction with the University of Loughborough, publishes Retirement Living Standards each year. These are widely used as benchmarks for what different lifestyles in retirement actually cost.

The PLSA defines three retirement lifestyles for a single person living outside London: minimum (£13,400 per year), moderate (£31,700 per year), and comfortable (£43,900 per year). These figures cover essentials, plus some discretionary spending appropriate to each tier.

Comparing these benchmarks against £250,000 of retirement savings: a £250,000 pot plus full State Pension (£22,000 per year combined) supports the minimum lifestyle comfortably, falls well short of the moderate benchmark, and is significantly below the comfortable level. The gap between £22,000 and the £43,900 needed for a comfortable single person retirement is over £20,000 per year, which represents a major lifestyle difference.

For couples, where both partners receive a State Pension and combine pension pots, the picture changes. Two State Pensions plus a £250,000 pension pot produces approximately £34,000 per year combined, comfortably exceeding the moderate lifestyle benchmark for a couple.

Can you retire on £250,000 if you retire later?

Time is the most powerful variable in retirement planning, and pushing back the retirement date by a few years has a much bigger effect than most people expect.

Consider someone aged 55 with a £250,000 pot. If they continue contributing £1,000 per month and the pot grows at 5% per year, by age 60 the pot will be approximately £383,000. By age 65, it will be approximately £555,000. By age 67 (current State Pension age), it will be approximately £632,000.

At £555,000 with the State Pension, the 4% rule produces a combined annual income of approximately £34,000 per year, which exceeds the moderate retirement benchmark for a single person. At £632,000 with the State Pension, the combined income is approximately £37,000 per year, getting closer to the comfortable benchmark.

The point is that £250,000 at age 55 is meaningfully different from £250,000 at age 65. If your pot is currently £250,000 and you have flexibility on the retirement date, the most powerful action you can take is to extend the working period and continue contributing. Five additional years of saving and growth can be the difference between a frugal retirement and a moderately comfortable one.

A recent example illustrates this well. A client, I’ll call her Margaret, came to us at age 56 with a £248,000 pension pot, having worked as a senior project manager for over thirty years. She was exhausted, hoping to leave work the following year, and worried whether her savings would stretch. When we built the cashflow model, the picture initially looked tight: drawing the £20,000 per year she felt she needed would have depleted her pot by age 67, just as the State Pension began. By rephasing her plan, working three more years on a reduced four day week, redirecting her bonus into pension contributions, and timing her tax free lump sum to bridge the gap to State Pension age, we modelled a sustainable income of around £24,000 per year through to age 90, with a meaningful buffer for unexpected costs. What changed for Margaret was not the size of the pot, but the clarity of the plan. She left our second meeting saying it was the first time in years she had felt genuinely calm about money.

Can you retire early on £250,000?

The honest answer is: usually not, unless you have other significant income sources or assets. £250,000 is rarely enough to support a 30 year retirement on its own from age 55 or 60.

Consider someone retiring at 55 on £250,000 with no other income until State Pension age (currently 66). They need to fund 11 years of retirement entirely from the pension pot before any State Pension begins. Withdrawing £20,000 per year from £250,000 (around 8%) for 11 years would deplete the pot completely before any State Pension started, even if the investments grew at 5% per year.

Withdrawing at a sustainable 4% rate would produce only £10,000 per year, which is below the minimum retirement lifestyle benchmark, particularly without the State Pension to supplement it.

Early retirement on £250,000 alone is therefore generally not realistic. It can work where there are other significant resources: an inheritance expected, rental income, a working partner, a small business income, or significant ISA savings outside the pension.

For someone in their mid forties or early fifties with £250,000 already saved, a more realistic plan often involves continuing to work and save until 60 or 65, by which point the combination of additional contributions, investment growth, and a closer State Pension start date makes the position substantially stronger.

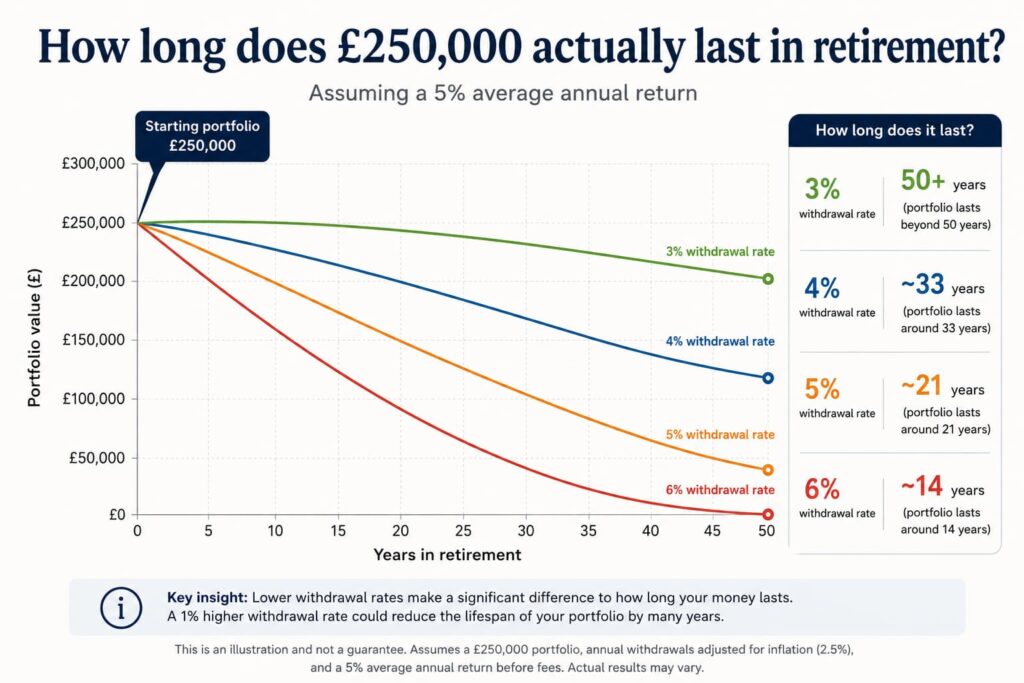

How long does £250,000 actually last in retirement?

The answer depends entirely on the withdrawal rate. The table below shows approximate longevity at different withdrawal rates, assuming average market returns of 5% per year and inflation at 2.5% per year.

Withdrawing 3% per year (£7,500 from £250,000): the pot is likely to last 35 years or more, often growing in real terms.

Withdrawing 4% per year (£10,000 from £250,000): the pot is likely to last around 30 years across most market scenarios. This is the classic Bengen 4% rule.

Withdrawing 5% per year (£12,500 from £250,000): the pot is likely to last 20 to 25 years, depending heavily on market returns in the early years (sequence of returns risk).

Withdrawing 6% per year (£15,000 from £250,000): the pot is likely to last 15 to 20 years, with significant risk of running out earlier if market returns are poor.

The 4% rule is not a guarantee. In particular, retiring just before a major market downturn (sequence risk) can deplete a pot faster than the rule suggests. Most cashflow planners use Monte Carlo simulations to model thousands of possible market scenarios and produce a probability of the pot lasting through retirement, which gives a more nuanced picture than a single rule.

What about the 25% tax free lump sum?

Under current UK pension rules, you can usually take up to 25% of your pension pot as a tax free lump sum (technically called the Pension Commencement Lump Sum, or PCLS). This is capped at £268,275 (or 25% of £1,073,100, the protected lifetime allowance figure).

On a £250,000 pot, this means up to £62,500 can be taken tax free. The remaining £187,500 stays invested and is drawn as taxable income, either through drawdown or through annuity purchase.

Whether to take the tax free lump sum upfront or spread it over time is a question that depends on your other income, your tax position, and what you intend to use it for. Taking it all at once is fine if you have a clear use (clearing a mortgage, gifting to family, buying property) or want certainty. Spreading it over several years can be more tax efficient if it allows the rest to keep growing in the tax wrapper.

In my experience, the right approach to the tax free lump sum depends almost entirely on a client’s wider circumstances rather than any general rule. I generally recommend taking it all at once when there is a clear, time sensitive purpose for the cash, clearing a remaining mortgage, helping adult children onto the property ladder, or funding a specific lifestyle goal in the early years of retirement when health and energy are highest. Where there is no immediate need, I usually suggest spreading it over several tax years, often by drawing it in stages alongside taxable income, so that more of the pot continues to grow inside the pension wrapper free of income tax, capital gains tax, and inheritance tax. The questions I ask clients to help them decide are practical ones: what would you actually do with the money in the next twelve months, what other taxable income will you have, do you have a partner whose tax position changes the picture, and how comfortable are you with investment risk on the money once it leaves the pension. The answers usually point clearly to one approach over the other.

What if your pot is below £250,000?

If you are reading this with a pot below £250,000 and feeling concerned, the first thing to know is that you have time to act, particularly if you are still in your forties or fifties.

Three actions tend to make the biggest difference:

First, consolidate any old workplace pensions. The Pensions Policy Institute estimates there are 3.3 million lost pension pots in the UK, worth a combined £31.1 billion. Consolidating old pots not only reduces administration but often reveals that you have more saved than you realised.

Second, increase contributions, particularly if you are in the 60% tax trap (earnings between £100,000 and £125,140). Pension contributions in this earnings band receive 60% effective tax relief, making them exceptionally efficient.

Third, review your investment strategy. A pot held in cash or low growth investments will produce a very different outcome at retirement than the same contributions invested in a diversified equity portfolio over 20 plus years. The single biggest determinant of long term pension outcomes after contribution rate is investment return, and that comes from getting the asset allocation right and keeping costs low.

Should you get a financial adviser if you have £250,000?

For most people approaching retirement with £250,000 or more, working with a financial adviser is genuinely worth the cost. The reason is not that retirement planning is impossibly complex, but that the consequences of small mistakes are large and irreversible.

Specific decisions where advice typically pays for itself include: when to take the tax free lump sum and how much to take, whether to use drawdown or an annuity (or both), how to coordinate pension income with the State Pension and any other income sources, how to manage tax efficiently in retirement, and how to structure the pot so it lasts the rest of your life.

Advice is typically not legally required for a £250,000 defined contribution pot. However, where the pot includes any defined benefit (final salary) element worth more than £30,000, or where there are guaranteed annuity rates, regulated advice is mandatory under FCA rules.

Frequently Asked Questions

Can I retire on £250,000?

It is possible to retire on £250,000, but the lifestyle it supports depends on whether you also receive the State Pension and when you retire. With the full State Pension, a £250,000 pot supports a frugal but reasonable retirement of around £22,000 per year for a single person. It is below the PLSA moderate retirement benchmark of £31,700 for a single person.

How much income will £250,000 give me in retirement?

At a 4% withdrawal rate, £250,000 produces approximately £10,000 per year before tax. After taking 25% as a tax free lump sum, the remaining £187,500 produces approximately £7,500 per year at 4%. Buying an annuity at 65 from £187,500 currently produces approximately £14,000 per year for life.

Can I retire at 55 with £250,000?

Generally no, unless you have other significant income sources. £250,000 alone is rarely enough to support a 30 year plus retirement starting at 55, particularly given the State Pension does not start until 66 (rising to 67). Most people in this position need to continue working until 60 or 65 to make the maths sustainable.

How long will £250,000 last in retirement?

At a sustainable 4% withdrawal rate, £250,000 should last around 30 years on average. At a 5% withdrawal rate it may last 20 to 25 years. At 6% it may last 15 to 20 years. The exact figure depends heavily on investment returns and market timing in the early years of retirement.

How much do I need to retire comfortably in the UK?

According to the PLSA Retirement Living Standards, a single person needs around £43,900 per year for a comfortable retirement, and a couple needs around £60,600 per year. To produce this level of income from a pension at a 4% withdrawal rate, plus the State Pension, you would need a pension pot of approximately £775,000 for a single person and £600,000 between a couple.

Can I get the State Pension and a private pension?

Yes. The State Pension is paid to anyone who has accrued sufficient National Insurance contributions (35 qualifying years for the full new State Pension), regardless of any private pension or other income. The State Pension is taxable, and it adds to any other taxable income for income tax purposes.

What is the 4% rule?

The 4% rule was developed by US economist William Bengen in 1994. It suggests that withdrawing 4% of your initial pension pot per year, adjusted for inflation, will likely make the pot last 30 years across most historical market scenarios. It is a useful starting point but not a guarantee, particularly if you retire just before a market downturn.

Should I consolidate my pensions before retiring?

Often yes, but not always. Consolidating reduces administration, can lower fees, and gives you a clearer picture of your overall position. However, you should never consolidate pensions with guaranteed benefits (such as guaranteed annuity rates or defined benefit pensions) without taking specialist advice.

Important: This article is for general information only and does not constitute personal financial advice. Tax treatment depends on individual circumstances and may change. Always speak to a qualified financial adviser before making decisions about your pension or retirement.

Sources used and citations

Pensions and Lifetime Savings Association (PLSA). Retirement Living Standards.

Saltus (2025). Can I retire with a £250k pension pot?

Unbiased (2025). What income would a £250,000 pension pot give me?

PensionBee. What is the 4% rule for withdrawals in retirement?

HMRC. Tax on your private pension contributions and Pension Commencement Lump Sum guidance.