If you are considering hiring a financial adviser for the first time, or if you are reviewing what you currently pay your existing adviser, the question of what is a reasonable fee is one of the most important you can ask. Most clients I speak to have a rough sense that they are paying around 1% or 2% of their portfolio per year, but very few can tell me exactly what that 1% or 2% covers, what it includes, what it excludes, and whether they are getting value for it.

This guide sets out what UK financial advisers actually charge in 2026, how the different fee structures work, what to expect for a portfolio of £250,000 or more, and how to assess whether the fee you pay represents fair value under the FCA’s Consumer Duty rules.

In my experience, the majority of clients who come to us have only a vague idea of what they are actually paying their existing adviser, and even fewer can articulate what they are receiving in return. The headline percentage matters far less than what sits behind it: the question is not whether 1% or 2% is the right number in the abstract, but whether the service, advice and outcomes delivered genuinely justify the fee being charged. What I have consistently seen in our own practice is that when fees are presented transparently and clearly tied to the work being done, clients understand them, accept them, and feel well served.

Table of Contents

ToggleHow are UK financial advisers paid?

UK financial advisers earn revenue in three main ways. The first is through a percentage of assets under management, often referred to as AUM fees. The second is through fixed fees for specific pieces of work. The third is through hourly rates for ad hoc advice.

By far the most common model in the UK is the percentage of assets under management. According to research published by Unbiased in February 2026, the vast majority of UK advisers use a percentage based fee structure. This typically ranges from 0.5% to 1% of the portfolio per year, with lower percentages applied to larger portfolios on a tiered basis. For pension transfer advice specifically, the FCA found in 2020 that the average initial advice fee was 2.4% of the amount transferred, with ongoing advice fees averaging around 0.8% per year.

Fixed fees are growing in popularity, particularly for clients with larger portfolios where a percentage based fee starts to look disproportionate. Hargreaves Lansdown publishes its initial advice fees as typically up to 2% of the value of the investment, while M&G’s published advice rate works on a tiered basis from 3% on the first £50,000 down to 1.5% on amounts above £200,000.

Hourly rates for financial advice typically range from £100 to £350 per hour for one off engagements, depending on the adviser’s experience and the complexity of the issue.

What is the typical total cost of financial advice in the UK?

The honest answer most advisers will not give you upfront is that the total cost of financial advice has multiple layers. The headline percentage fee is only the start. The total cost a client actually pays sits across four components.

First, the adviser fee itself. This is what the adviser earns. For ongoing advice, this typically sits between 0.5% and 1% per year on a percentage based model, or a fixed retainer of between £2,000 and £10,000 per year for fixed fee firms.

Second, the platform fee. This is what the investment platform charges to administer the underlying investments. Platform fees typically range from 0.15% to 0.45% per year, often tiered down on larger portfolios.

Third, the fund charges. The funds the adviser invests in carry their own annual costs, known as Ongoing Charges Figures (OCF). For passive index funds, the OCF can be as low as 0.05% to 0.20%. For actively managed funds, the OCF typically ranges from 0.5% to 1.5%.

Fourth, transaction costs. Each time the portfolio is rebalanced or new funds are purchased, there can be small dealing costs and bid offer spreads. These typically add 0.05% to 0.20% per year on a managed portfolio.

Adding these together gives you a total annual cost. For a typical UK adviser using a portfolio of actively managed funds, the total annual cost often sits between 1.5% and 2.2%. For an adviser using mostly passive funds on a low cost platform, the same total can be as low as 0.7% to 1%. The difference is significant: on a £400,000 portfolio, the difference between 0.85% and 1.85% is £4,000 every year, compounding into well over £100,000 over a 20 year horizon.

What are the fees at the major UK firms?

The clearest way to put fees in context is to compare published fee structures across some of the largest UK wealth managers.

St. James’s Place implemented a new charging structure on 26 August 2025. Initial advice fees are tiered: 3% on the first £250,000 invested, 2% on the next £250,000, and 1% on amounts above £500,000, capped at £30,000. Ongoing advice fees are 0.8% per year. Ongoing product charges are 0.35% per year on the first £500,000 in bonds and pensions, tapering down. Total ongoing fees including funds typically work out at around 1.67% per year, by SJP’s own estimate. SJP advisers are restricted, meaning they can only recommend SJP’s own products and funds.

Hargreaves Lansdown (HL) charges initial advice fees of up to 2% of the investment, with ongoing advice charged at 0.365% (+VAT where applicable, and minimum charges apply). HL platform fees are tiered from 0.45% on the first £250,000 down to 0% on amounts over £2 million. HL operates as a whole of market firm.

M&G Wealth charges initial advice fees on a tiered basis from 3% on the first £50,000 down to 1% on amounts above £500,000.. Ongoing advice fees vary by service tier.

A typical independent financial adviser (IFA) operating outside the major networks tends to charge initial fees of 1% to 3% on a tiered basis, with ongoing fees of 0.5% to 1% per year. Total ongoing costs including platform and funds for an IFA model typically come in at 1% to 1.5% per year.

Boutique whole of market firms working with HNW clients on £250,000 plus portfolios often offer total ongoing costs at the lower end of this range, particularly when using a mix of passive and selectively chosen active funds and a competitively priced platform.

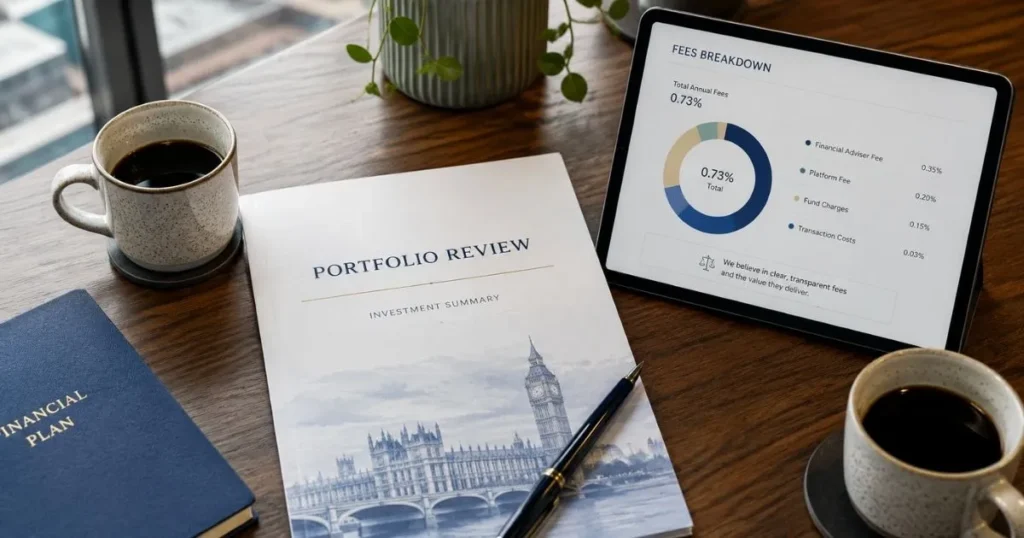

At Ark Wealth Management, our ongoing advice fee is 1% per year, which sits within the typical range for full-service UK wealth managers and well below SJP’s headline initial charges and total ongoing cost of around 1.67%. We have chosen to keep our pricing simple and consistent rather than tier it through layers of separate product, platform and advice charges. What that 1% covers is deliberately broad: ongoing investment management, full financial planning across tax, pensions, protection and estate considerations, regular review meetings, and direct access to your adviser whenever you need us. We have structured fees this way because we believe the client should be able to see, in a single number, what they are paying and exactly what they are getting in return, and because aligning our fee to the value of the portfolio keeps our incentives aligned with growing your wealth over the long term.

What is fair value under the FCA's Consumer Duty?

Since July 2023, all UK financial firms have been subject to the FCA’s Consumer Duty, which introduces a higher standard of protection for retail clients. One of the four core outcomes of the Consumer Duty is the requirement that firms deliver fair value.

Fair value, in the FCA’s framework, is not the same as cheap. The FCA explicitly states that its rules do not set prices, do not require prices to be low, and do not require firms to charge the same as competitors. What fair value does require is that the price a customer pays is reasonable in relation to the benefits they receive, and that firms can demonstrate this with evidence.

In practice, this means firms have to be able to answer the question: what is the client getting for the fees they are paying? An ongoing advice fee should correspond to a documented ongoing service. A higher fee is justifiable where the service is genuinely more comprehensive or specialised. A higher fee is not justifiable simply because the firm has historically charged it.

The FCA’s review of the largest 20 UK wealth managers, published in February 2025, found that 83% of cases sampled showed advisers had conducted suitability reviews, 15% had been offered but not responded to or declined by the client, and 2% had received no contact from their adviser at all. The 2% figure becomes significant when applied to large client bases: across SJP’s client base of approximately 900,000, this is potentially tens of thousands of clients who may not have been receiving the ongoing service their fees were paying for.

The lesson for any client paying ongoing advice fees is to ensure you can clearly identify the service you are receiving in return. If you cannot, the fair value test is not being met.

How should you compare fees between firms?

The most practical comparison is the total ongoing annual cost as a percentage of your portfolio. This is the figure that matters for your long term wealth, because it is the amount that compounds against you every year.

To make a fair comparison, you need to add together the four components: adviser fee, platform fee, fund charges, and any transaction costs. Some firms will quote you only the adviser fee, which can make their proposition look much cheaper than it is in reality. The figure you want is the total ongoing annual cost in pounds, presented in writing.

Most reputable firms will provide this as a standard part of their proposition. If a firm is reluctant to give you a clear total annual cost figure, that is a strong signal to look elsewhere.

A useful sense check is to calculate the impact of fees over a 20 year horizon. On a £500,000 portfolio growing at 5% per year before fees, a 2% total annual cost results in a final pot of approximately £810,000. The same portfolio at a 1% total annual cost results in approximately £980,000. The difference, £170,000, is the cost of the higher fee compounded over time. This kind of calculation, done in writing before signing any agreement, makes the value question concrete in a way that headline percentages do not.

To make this concrete, consider an illustrative comparison for a £500,000 portfolio. At Ark, on our flat 1% ongoing advice fee, the client pays £5,000 per year in adviser charges, with platform and fund costs typically adding around 0.30% to 0.45% depending on the underlying portfolio mix, giving a total ongoing cost of roughly 1.30% to 1.45% per year, or £6,500 to £7,250. The same client at SJP, on its published total ongoing cost of around 1.67% per year, would pay approximately £8,350 per year. Over a 20 year horizon, on a portfolio growing at 5% before fees, that difference of around £1,100 to £1,850 per year compounds into tens of thousands of pounds of additional cost. The point is not that the SJP service has no value, but that the practical difference between fee structures is significant once it is laid out in pounds rather than percentages, and clients deserve to see that calculation in writing before they commit.

Are fixed fees better than percentage fees?

This is one of the most discussed questions in UK financial advice, and the honest answer is that it depends on the size of your portfolio and the complexity of your needs.

For a portfolio of £250,000, a 1% ongoing advice fee equates to £2,500 per year. For a portfolio of £1,000,000, the same percentage equates to £10,000 per year. The actual amount of work the adviser does for the £1,000,000 client is rarely four times the work for the £250,000 client. As portfolios grow, percentage based fees can begin to look disproportionate to the actual service delivered.

Fixed fees, by contrast, charge a flat amount per year regardless of portfolio size. For HNW clients, this often works out cheaper, more transparent, and more aligned with the actual service being delivered. A fixed fee of £6,000 per year, for example, equates to 0.6% on a £1,000,000 portfolio and 1.2% on a £500,000 portfolio. The fixed fee model becomes more attractive as the portfolio grows.

The trade off is that fixed fees can be off putting at the start of a relationship because they look like a large number in absolute terms, even if they are economical in percentage terms. The choice between fixed and percentage based pricing should always be modelled against the specific circumstances of the client.

What questions should you ask before agreeing to fees?

Before you sign any client agreement, there are seven questions you should ask in writing and have answered in writing.

First: what is the total annual cost as a percentage of my portfolio, including adviser fees, platform fees, fund charges, and transaction costs? You want a single figure expressed both as a percentage and in pounds for your specific portfolio size.

Second: are you whole of market or restricted? If restricted, what range of products and providers can you recommend, and what falls outside that range?

Third: what is included in the ongoing advice fee? You want a written list of services delivered each year. At a minimum, this should include an annual review meeting, portfolio rebalancing, proactive communication on tax and regulatory changes, and accessibility for ad hoc questions.

Fourth: are there any exit fees or lock in periods? If yes, exactly how much would I pay if I left in year one, year two, year three, year five?

Fifth: do you charge initial fees, and if so, on what basis? On a tiered basis or flat percentage? Capped or uncapped?

Sixth: who will I actually be working with? Will my named adviser be the person making investment decisions and reviewing my plan, or am I being passed to a junior or a centralised team?

Seventh: how do you assess whether my fees represent fair value under the FCA Consumer Duty? A confident, well prepared adviser should have a clear answer to this.

Frequently Asked Questions

What is the average financial adviser fee in the UK?

According to Unbiased’s February 2026 research, most UK advisers charge between 0.5% and 1% of assets under management per year. The FCA’s previous research, conducted in 2020, found average initial advice fees of 2.4% of the amount invested and average ongoing advice fees of 0.8% per year. Whole of market and independent advisers typically sit at the lower end of these ranges.

How much does a financial adviser cost in the UK in 2026?

For a £400,000 portfolio, the typical total annual cost (advice fee, platform fee, fund charges) ranges from approximately £3,400 (0.85%) at a low cost whole of market firm to approximately £6,600 (1.65%) at a major restricted firm. For a £1,000,000 portfolio, the same range is approximately £8,500 to £16,500 per year.

What is the difference between fixed fee and percentage fee advisers?

Percentage fee advisers charge a percentage of the portfolio they manage. Fixed fee advisers charge a flat amount per year regardless of portfolio size. For larger portfolios (typically £750,000 or more), fixed fee structures often work out cheaper. For smaller portfolios, percentage based fees usually work out cheaper. The right choice depends on your portfolio size and the complexity of your needs.

How much does it cost to hire a financial adviser for a one off pension review?

A one off pension review or pension transfer recommendation typically costs between £1,500 and £3,500, depending on complexity. For defined benefit transfers requiring specialist advice, fees can be higher, often £3,000 to £5,000.

What is included in an ongoing advice fee?

At a minimum, an ongoing advice fee should cover an annual review meeting, portfolio rebalancing, proactive communication about tax and regulatory changes, and accessibility for ad hoc questions throughout the year. Anything less than this would not generally be considered fair value under the FCA’s Consumer Duty rules.

Are SJP fees higher than independent advisers?

Generally yes. SJP’s total ongoing fees, by SJP’s own estimate, are around 1.67% per year on a typical portfolio. Whole of market independent advisers typically charge 1% to 1.5% in total ongoing fees on a comparable portfolio. The difference of 0.5% to 0.7% per year, compounded over decades, results in significantly different long term outcomes.

Can I negotiate financial adviser fees?

Yes, often. Many advisers, particularly at the largest firms, have some discretion to negotiate fees, especially for HNW clients with portfolios above £500,000. The FCA’s Consumer Duty does not prevent firms from negotiating, and many firms will quietly reduce headline fees to win or retain a client. It is always worth asking.

How do I know if I am paying fair value for financial advice?

The fair value test under the FCA’s Consumer Duty is whether the price you pay is reasonable in relation to the benefits you receive. The most practical question to ask yourself is: can I clearly identify the services I receive in return for my ongoing fee? If the answer is no, or if the service consists of little more than an annual letter, the fair value test is unlikely to be met.

Important: This article is for general information only and does not constitute personal financial advice. Tax treatment depends on individual circumstances and may change. Always speak to a qualified financial adviser before making decisions about your investments.

Sources used and citations

Unbiased (2026). Financial adviser fees: How much does a financial adviser cost?

Financial Conduct Authority. Consumer Duty rules and Our Consumer Duty focus areas 2025/26.

Financial Conduct Authority Handbook, PRIN 2A.4 (Consumer Duty fair value rules).

MoneyHelper. Financial adviser fees.

Hargreaves Lansdown. Financial advice charges.

M&G Wealth. Advice costs and charges.

MoneyWeek (2025). St James’s Place confirms new fees: what it means for customers.

Tideway Wealth (2024). St James’s Place: exit fees are on the way out.