If you earn over £100,000 a year but find yourself wondering where the money goes each month, you are not alone. Research published by Killik in July 2025 found that nearly half of UK earners on six figure salaries (48%) expected to feel more financially comfortable than they actually do. Almost a third (31%) feel pressure to earn more because they have no financial safety net, despite being in the UK’s top 2% of earners.

There is a name for this. You are a HENRY: a ‘High Earner, Not Rich Yet’. The term was coined by Fortune magazine writer Shawn Tully in 2003 to describe people earning impressive salaries who somehow could not seem to build the wealth their income should produce. Two decades later, the HENRY phenomenon is more relevant than ever, particularly in the UK, where high tax thresholds, expensive housing, and complex pension rules conspire to make wealth building harder than the headline salary suggests.

This guide explains what being a HENRY actually means in the UK in 2026, why so many high earners struggle to build wealth, and the specific financial planning steps that move you from ‘high earning’ to ‘genuinely wealthy’.

At Ark, I see HENRYs nearly every week, and most are professionals in their mid-thirties to mid-forties juggling demanding careers, young families, and surprisingly tight monthly cashflow. The pattern I notice first is almost always the same: strong income, scattered savings across legacy workplace pensions and a cash ISA, and very little long-term structure tying it all together. By the time they reach out, they usually sense they should be further ahead than they are, and what they really need is a clear plan rather than another product.

Table of Contents

ToggleWhat is a HENRY?

In UK financial planning, a HENRY is typically someone earning £100,000 or more, often well above this, but who does not yet have the assets and savings you would expect at that income level. They are often in their thirties or early forties, in senior roles in finance, law, technology, consulting, or medicine, and on paper they look successful. The reality is often different.

Several factors define the typical UK HENRY. First, they earn well, often £150,000 to £400,000 per year. Second, they pay a lot of tax: the UK’s 60% effective tax trap between £100,000 and £125,140 is a particular challenge for this group. Third, they have significant outgoings: large mortgages, high childcare costs, expensive city lifestyles, and often education costs for children. Fourth, they have built less wealth than their income would suggest, with workplace pension pots, ISA savings, and other investments often falling short of where they should be.

The Killik research found that 87% of HENRYs have children, 58% have partners who depend on them financially, and almost a third (31%) also support their parents financially. Many are also in the position of not standing to inherit significantly from their own parents, putting more pressure on their own earnings to fund their lifetime needs.

Why do high earners struggle to build wealth?

There are five structural reasons why earning a six figure salary in the UK does not automatically translate into wealth.

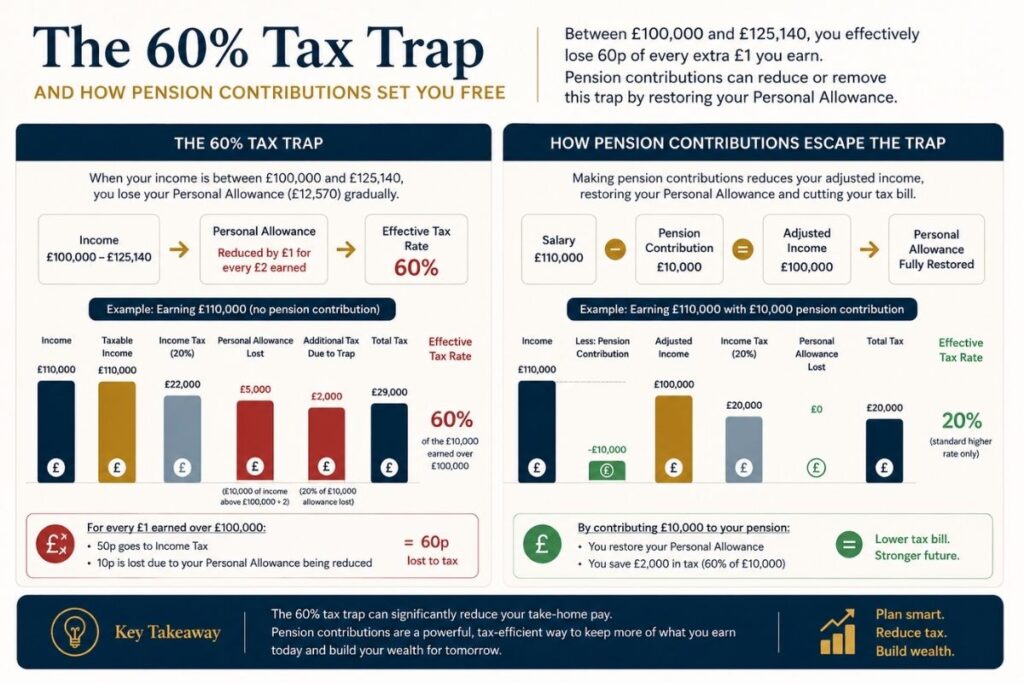

First, the 60% tax trap. In the UK, individuals earning between £100,000 and £125,140 lose £1 of personal allowance for every £2 they earn over £100,000. This creates an effective marginal tax rate of 60% in this band. Combined with employee National Insurance, this means a HENRY in this earnings band keeps roughly 38p of every additional £1 they earn. The psychological effect of this is significant: pay rises and bonuses do not feel rewarding because most of the increase is lost to tax.

Second, lifestyle creep. As earnings rise, expectations rise to match. The £80,000 salary that felt comfortable becomes the £200,000 salary that still feels stretched. Bigger houses, school fees, club memberships, holidays, cars: each individual decision is rationalisable, but cumulatively, lifestyle creep absorbs the additional income before it ever reaches savings.

Third, the cost of family. Childcare in London for two children can easily exceed £40,000 per year. School fees for two children at a good independent school can exceed £60,000 per year. Mortgages on family homes in HNW catchment areas can run £4,000 to £8,000 per month. None of these costs is unique to HENRYs, but the combination is particularly heavy on this group.

Fourth, complex tax position. HENRYs frequently encounter the tapered annual allowance for pensions, the Restricted Annual Allowance for those who have flexibly accessed defined contribution pensions, the High Income Child Benefit Charge, the loss of personal allowance, and the High Income Stamp Duty surcharge on second properties. Without specialist advice, it is very easy to miss legitimate tax efficient strategies, or to inadvertently trigger penalties.

Fifth, lack of planning structure. Many HENRYs are deeply competent in their professional fields but have given little structured thought to their personal finances. Money flows in and out without a plan. Pensions sit untouched in old workplace schemes. Investments accumulate without a clear strategy. Hard work compensates for lack of planning, but the long term cost is significant.

The most common ‘aha’ moment I see at Ark is when a HENRY watches their full financial picture modelled out for the first time. People walk in assuming the answer is to earn more or invest more aggressively, but the screen usually tells a different story: the real gains come from tax structure, pension allowances, and disciplined cashflow rather than chasing returns. After that meeting, behaviour tends to shift quickly. Clients stop reacting to short-term market noise, start automating contributions, and begin treating their plan as the engine and their lifestyle as the output, not the other way around.

How can a HENRY escape the 60% tax trap?

The 60% tax trap between £100,000 and £125,140 is the single most expensive piece of the UK tax code for HENRYs, and it is also the one that responds most readily to planning. The mechanism is set out in section 35 of the Income Tax Act 2007: for every £2 of adjusted net income above £100,000, you lose £1 of personal allowance, until the personal allowance is fully withdrawn at £125,140. HMRC’s published guidance confirms the practical effect, namely an effective marginal tax rate of 60% in this earnings band. The most powerful tool for HENRYs to manage this is pension contributions.

If you earn £125,140 and contribute £25,140 to a pension (taking your taxable income back to £100,000), you receive 60% effective tax relief on that contribution: 40% tax relief at higher rate, plus you reclaim the personal allowance you would otherwise have lost. In practical terms, contributing £25,140 to a pension costs you £10,056 net, with the remaining £15,084 effectively funded by tax relief. This is one of the few situations in the UK tax code where the marginal return on a financial decision is genuinely 60%.

The Annual Allowance for pension contributions in 2025/26 is £60,000, including any employer contributions. The Tapered Annual Allowance, set out in section 228ZA of the Finance Act 2004 (as amended by subsequent Finance Acts), reduces the standard allowance for those with high adjusted income. If your threshold income exceeds £200,000 and your adjusted income exceeds £260,000, the allowance reduces by £1 for every £2 of adjusted income above £260,000, down to a minimum of £10,000 at adjusted income of £360,000. Working out exactly how much you can contribute requires careful analysis of your total income, employer contributions, and use of carry forward from previous years.

Carry forward, set out in section 228A of the Finance Act 2004, is particularly valuable for HENRYs. It allows you to use unused pension Annual Allowance from the previous three tax years, provided you were a member of a registered pension scheme during those years. For a HENRY who has been earning well but not maximising pension contributions, carry forward can unlock the ability to contribute up to £180,000 in a single year on top of the current year’s allowance.

This kind of multi year tax planning is exactly the type of work that pays for itself many times over and is often overlooked by people without a structured financial plan.

What other tax-efficient tools should a HENRY be using?

Beyond pension contributions, there are several other tax efficient wrappers HENRYs should be using systematically.

ISAs allow you to contribute up to £20,000 per year per individual into a tax wrapper that protects all future growth from capital gains tax and dividend tax. For couples, this is £40,000 per year, and for a couple maximising ISAs over 20 years, the ISA wrapper alone can build a tax free pot well into seven figures.

Junior ISAs allow up to £9,000 per year per child to be saved tax efficiently for their future. For HENRYs supporting children’s education and first home costs, building Junior ISAs from birth produces meaningful pots by adulthood.

EIS (Enterprise Investment Scheme) and SEIS investments offer significant tax reliefs for HENRYs willing to invest in higher risk early stage companies. Income tax relief of 30% (EIS) or 50% (SEIS), capital gains tax deferral or exemption, and inheritance tax relief after two years can make these powerful tools, though they involve genuine risk and should only be considered after the foundational layers of pensions and ISAs are maximised.

VCTs (Venture Capital Trusts) offer a similar structure with 20% income tax relief on contributions of up to £200,000 per year, tax free dividends, and tax free growth on disposal. VCTs are listed on the London Stock Exchange and provide more diversification than direct EIS investments.

Salary sacrifice arrangements through your employer can convert taxable salary into pension contributions, electric vehicles, or cycle to work schemes, saving both income tax and National Insurance. For a HENRY in the 60% tax trap, salary sacrifice into the pension is doubly attractive because it saves both the high marginal income tax and National Insurance simultaneously.

A typical first engagement at Ark begins with a discovery conversation, where we map out income, tax position, debts, protection, pensions, ISAs, and any equity or bonus structures in one place. From there, we model the next ten to twenty years under different saving, tax, and lifestyle scenarios, so the client can see the trade-offs in pounds rather than abstractions. The early wins are usually consolidating old pensions, switching on carry forward where appropriate, restructuring ISA contributions for a couple, and adding the protection most HENRYs quietly know they are missing. Twelve to twenty-four months in, the picture looks calmer: contributions are automated, tax is handled proactively each year, the investment strategy matches the actual goals, and the client has stopped wondering whether they are doing the right thing.

How much should a HENRY actually be saving?

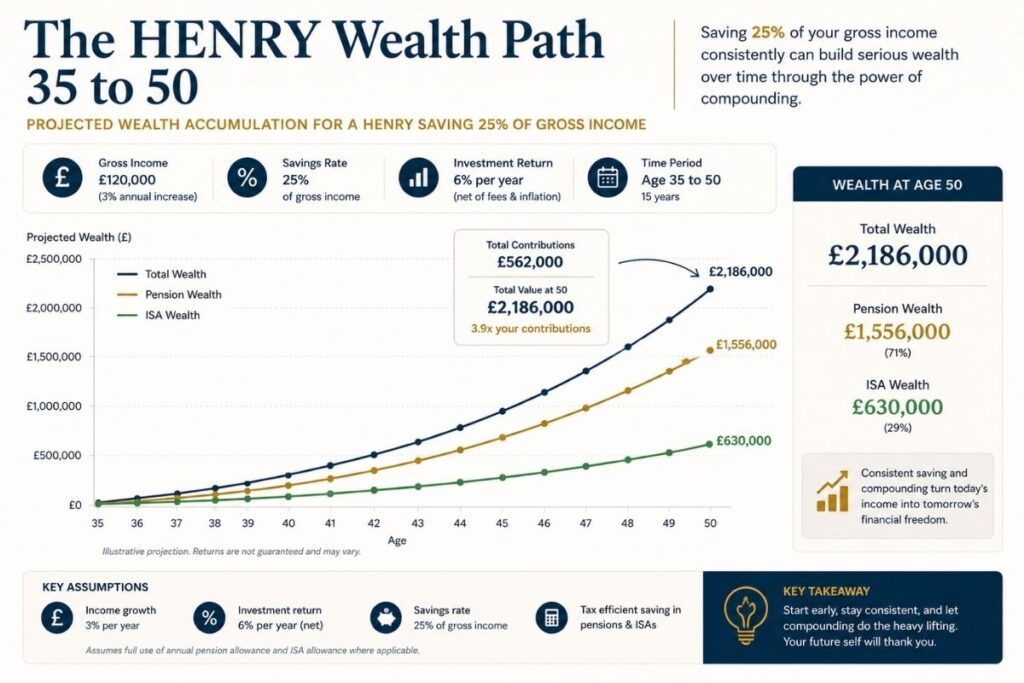

A useful rule of thumb is that a HENRY in their thirties should aim to save 20% to 30% of gross income across pensions, ISAs, and investments. For someone earning £200,000, that is £40,000 to £60,000 per year. This sounds high, but viewed across the full set of wrappers (pension, ISA, employer matching, salary sacrifice), it is achievable for most HENRYs without a dramatic lifestyle change.

By age 50, a HENRY who has saved at this rate consistently from their thirties should have built a meaningful pension pot, often £500,000 to £1,500,000, alongside ISA wealth and other assets. This is the point at which the HENRY label stops applying. The transition from ‘high earner not rich yet’ to genuinely wealthy is mathematical: saving and compounding from a high earnings base, sustained over 15 to 20 years, produces real wealth.

The risk for HENRYs who do not save at this rate is that their high earnings continue but the wealth never accumulates. By age 60, the gap between their earnings and their assets remains enormous, and retirement requires either continuing to work, drastic lifestyle reduction, or both.

What changes when you stop being a HENRY?

The transition from HENRY to genuinely wealthy is not just financial. It is psychological. HENRYs typically have a feeling of needing to keep earning to maintain their lifestyle. The transition point is when the wealth itself produces enough income, alongside more controlled drawdown from earnings, to fund the desired lifestyle.

Practically, this transition happens when investment income, pension drawdown, and other passive sources can cover desired annual expenditure. For a HENRY targeting £80,000 to £120,000 of annual retirement income, the wealth required is typically £2 million to £3 million, applying a 4% safe withdrawal rate.

Reaching this point earlier, ideally by mid to late fifties, gives HENRYs the genuine financial security their high earnings always promised but rarely delivered without a plan.

Frequently Asked Questions

What does HENRY stand for?

HENRY stands for High Earner, Not Rich Yet. The term was coined in 2003 by Shawn Tully, a writer at Fortune magazine, to describe people who earn high incomes but have not yet built significant wealth. In the UK, HENRYs are typically defined as those earning £100,000 or more.

What is the salary of a HENRY in the UK?

In the UK, the typical HENRY earns £100,000 or more. Many HENRYs earn considerably more, often £150,000 to £400,000, but the defining feature is the gap between income and accumulated wealth, not the absolute salary level.

Why is being a HENRY hard in the UK?

UK HENRYs face several specific challenges: the 60% effective tax rate between £100,000 and £125,140, the cost of family living in HNW catchment areas, large mortgages, complex pension rules including the Tapered Annual Allowance, and the absence of inherited wealth in many cases. These factors combined mean high incomes do not translate into wealth as quickly as headline numbers suggest.

How much should a HENRY save each year?

A useful rule of thumb is 20% to 30% of gross income across all tax efficient wrappers (pension, ISA, employer matching, EIS or VCT where appropriate). For someone earning £200,000, this means £40,000 to £60,000 per year of structured saving. Achieving this typically requires using pension contributions to manage the 60% tax trap and maximising ISA allowances.

What is the 60% tax trap and how do I avoid it?

In the UK, individuals earning between £100,000 and £125,140 lose £1 of personal allowance for every £2 they earn above £100,000. This creates an effective marginal tax rate of 60% in this band. The most effective way to avoid it is to contribute to a pension, reducing your adjusted net income back below £100,000. Pension contributions in this band receive an effective 60% tax relief, making them exceptionally tax efficient.

When does a HENRY stop being a HENRY?

A HENRY transitions to genuinely wealthy when accumulated wealth, alongside more managed earnings, can sustainably fund their lifestyle. For a typical HENRY targeting £80,000 to £120,000 annual retirement income, this requires accumulated wealth of £2 million to £3 million. Reaching this point typically requires consistent saving across pensions and ISAs from the thirties onwards.

Do HENRYs need a financial adviser?

Most HENRYs benefit significantly from structured financial advice because their tax position is complex and their income is high enough that small inefficiencies have large absolute consequences. A good adviser can identify pension carry forward opportunities, manage the Tapered Annual Allowance, structure ISA, EIS, and VCT contributions appropriately, and produce cashflow models that show how current decisions affect long term outcomes.

Important: This article is for general information only and does not constitute personal financial advice. Tax treatment depends on individual circumstances and may change. Always speak to a qualified financial adviser before making decisions about your investments or tax planning

Sources used and citations

Killik & Co (2026). Why it’s hard being a HENRY: research findings.

Chase UK (2024). Are you a High Earner, Not Rich Yet?

HMRC. Pension Annual Allowance and tapered annual allowance guidance.

HMRC. Personal Allowance: how it works.

Income Tax Act 2007, section 35 (personal allowance withdrawal).

Finance Act 2004, sections 228ZA and 228A (Tapered Annual Allowance and Carry Forward).

Tully, S. (2003). The Rich and How They Got That Way. Fortune Magazine.

Courtiers Wealth Management (2025). The rise of the UK HENRY.